[vc_row][vc_column][vc_video link=”https://www.youtube.com/watch?v=qPFs_1FQUg0″][vc_raw_html]JTNDZGl2JTIwaWQlM0QlMjJidXp6c3Byb3V0LXBsYXllci03MTkzODAzJTIyJTNFJTNDJTJGZGl2JTNFJTBBJTNDc2NyaXB0JTIwc3JjJTNEJTIyaHR0cHMlM0ElMkYlMkZ3d3cuYnV6enNwcm91dC5jb20lMkY4MTYyMyUyRjcxOTM4MDMtZGlnaXRhbC1iYW5raW5nLXRyZW5kcy1pbi0yMDIxLXBhcnQtMS5qcyUzRmNvbnRhaW5lcl9pZCUzRGJ1enpzcHJvdXQtcGxheWVyLTcxOTM4MDMlMjZwbGF5ZXIlM0RzbWFsbCUyMiUyMHR5cGUlM0QlMjJ0ZXh0JTJGamF2YXNjcmlwdCUyMiUyMGNoYXJzZXQlM0QlMjJ1dGYtOCUyMiUzRSUzQyUyRnNjcmlwdCUzRQ==[/vc_raw_html][/vc_column][/vc_row][vc_row][vc_column][vc_column_text]

Digital Banking Trends in 2021: Part 1

Welcome to the Executive Innovation Show Podcast, brought to you by One Touch Video Banking. During this podcast hear host Carrie Chitsey, talk about digital banking trends in 2021. Listen to this episode of The Executive Innovation Show Podcast as we discuss how banking has changed significantly in the past 12 months and what’s on the horizon.

Carrie Chitsey led the CRM Financial Services practice in Big 5 Consulting and then went on to own a financial services contact center. She has advised some of the largest banks in the US.

Since founding one of the first mobile companies in the US in 2008, she is known in the industry as a leader in digital/mobile innovation.

Named Top 50 Mobile Executives in the US, Top 100 Female Founders, and Top 40 Marketing Execs in the US. She hosts a podcast “The Executive Innovation Show” and is published in many magazines and online resources.

Learning Lessons From COVID

Digital is Key

What did COVID teach banks? The number one lesson that was learned is that digital is key and video is key. Banks learned that they have to have not just a contingency plan, but a plan in place for their employees to work remotely and digitally, which has never really been done in banking before.

Bank executives across the country learned that they need to have digital plans, both from the acquisition side of getting new customers and the servicing side from customer service and a retention perspective.

Updated Branch Design & Reduction

Another lesson learned is branch design. There has been so much time spent in banking trying to change branch layouts over the last few years to be this more open and inviting environment for customers to want to come in. This was to combat that people weren’t coming into the branch anymore and numbers were going down with digital technology.

Now branches have to look at how to now change that again to keep employees and customers safe. It’s time for glasses back up and a not so open environment. We’ll see in 2021, banks looking at it if they want to spend two to five million on physical branches given what they just learned from a digital perspective.

Digital Acquisition is a Necessity for All – Community Banks and Credit Unions Included

We’ve seen all over the news from the FDIC, bank numbers are down dramatically. A lot of that has to do with banks that were not prepared to acquire customers digitally. For community banks and credit unions, while doing digital marketing is still required, you come into a physical location to show that driver’s license to sign documents.

Historically digital sales from banks in the US were less than 10% of their acquisition. Your top global banks, it was upwards of 27%. So those banks thrived while your local and community banks still struggle. When those numbers come out for 2020 and 2021, we’re going to see a big shift in those numbers.

Banking Trends in 2021

Virtual Workforce

Banks historically didn’t want employees working from home because of security requirements. Now we’re seeing banks do more with fewer employees for those that had to furlough their employees. Your essential tellers and things like that will stay in physical locations, but as we look at relationship managers, business lending, loan officers, and more, we’re going to see a shift to working in a hybrid model. Maybe they work from home for a few days and in the branch other days. A lot of times these folks were already out on the road going and seeing customers trying to build community relationships. We’ll see more of a virtual workforce now that banks have seen that it can work.

Remote Advice

In 2015, McKinsey reported on what percentage of U.S. customers wanted remote advice, whether that’s wealth management, investments, or anything like that. They found out that 41% of U.S. customers wanted remote advice. That was five years ago. In 2019, less than 22% of banks offered remote advice through video or phone. In 2021, we’re going to see a lot of remote advice. As we look at those high margin products, servicing high net worth individuals, a lot of people have moved from their local demographic. Businesses are relocating entire headquarters from California to Texas. Customers and members might not be in a position where you’re by your local bank. And a lot of people need financial advice right now with the PPP loans, with financial struggles, things like that.

You have to have a remote advice strategy using video to still keep that face to face interaction. This allows you to service those customers because a large percentage of them aren’t in your driving distance anymore.

Video Banking

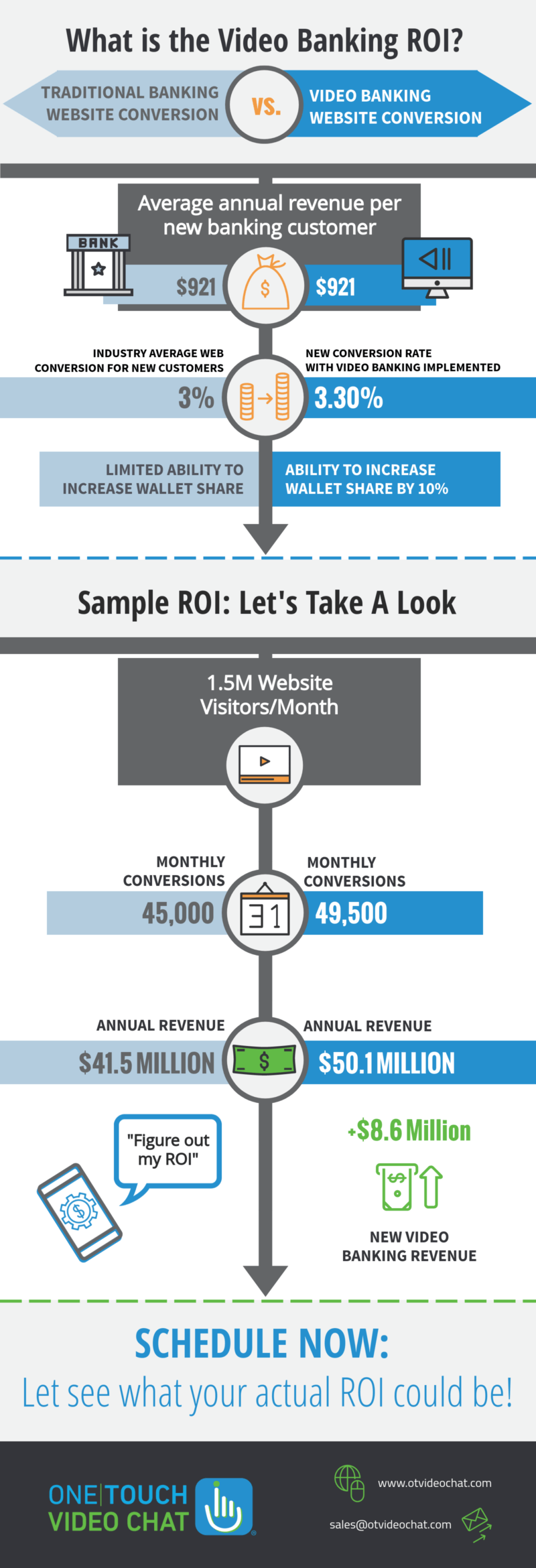

Every industry has seen such a rise in video and video conferencing. From school to work meetings, most people are now comfortable being on video. Having those video interactions from a banking perspective can move the needle on the acquisition side, increasing conversion rates by 3X. Video banking can help you with your NPS and C-SAT scores while increasing wallet share by up to 20%.

Your customers are not only banking with you, they’re banking with others. They’re banking with others because it’s easy and they’ve got long hours because they’re digital. And so you have to have video banking to compete on the acquisition side.

More importantly, on the servicing side, to be able to increase wallet share and retention. The average bank doesn’t profit off customers for three-plus years. So acquiring those customers, you can spend as much money as you want, but you have to retain them. Having those virtual face-to-face relationships, it’s going to increase that retention.

It will also help with relationship management, most relationship managers by default industry-wide, focus on that 20% of their customer base that has the money that’s coming in, that they have the relationship with. And the other 80% of those customers, they might reach out to them once a year, maybe twice a year, but they don’t have a good relationship with them. Get that 80% on video banking schedule, update calls, develop that relationship face to face, be proactive, and stay top of mind.

If you do that through video banking, that wallet share is going to go up dramatically. Those customers that are banking with three to five different financial institutions, they’re going to remember you on that face to face video call versus the guy next door that’s making a phone call.

Digital Footprint

As we talk about the acquisition side, acquiring new customers, the conversion rate is key. It doesn’t matter how many applications are started online. It’s what’s finished and what converts. You need a strategy where if people are starting applications and abandoning, you have to reach out to them. You have to set up and start scheduling video meetings. By having live video banking on your website, if somebody has questions about products, they can literally click “I need to talk to a business banker now”. Boom, you’re there face to face and that by itself can drive that conversion rate regardless of how much money you’re spending on the acquisition.

The typical acquisition is less than 1% on the conversion rate. The only way to increase that is you have to have that digital workflow that allows them to start and finish and acquire customers online. It can be assisted through a video banker, but it can’t be a situation where they start and then they have to come in. Your conversion rate will drop off.

If we go back down to state closures, people are going to want to open accounts, do everything online and not have to come in physically to keep themselves safe and to keep you safe. During pre-COVID, it was a convenience factor, and today convenience is still king, as well as safety.

The Time for Change is Now

Most banks, most employees have been in the banking world for their entire career. The online-only banks that are thriving have brought people in from other industries such as retail. You have to stop thinking like a four-wall brick and mortar bank and start thinking about virtually extending hours, acquiring customers beyond your driving distance to make up some of those margins, and expanding in the current times that we live in. If you don’t have that digital strategy in place, it should definitely be a top priority.

For more tips on how to grow from a servicing perspective – increasing wallet share, retention, NPS, C-SAT, acquisition perspective, and to learn how to reach people better while developing higher conversion rates, subscribe to the podcast. Stay tuned for all the special guests we have coming in 2021. And we look forward to helping you make 2021 great and a heck of a lot greater than 2020. Stay tuned for the next episode.

If you have any questions for this podcast if you want to ask our next guests that are coming up, feel free to submit questions, let us know what you want to hear for the banking podcast in 2021.

Download the playbook and stay tuned to our weekly episodes of the Knowledge Knugget to learn more best practices and tips on how to incorporate video banking and digital transformation into your bank or credit union.

Listen to the video banking podcast and subscribe to the podcast and rate us! Have a Knowledge Knugget idea? Reach out and submit today.

[/vc_column_text][/vc_column][/vc_row][vc_row][vc_column][g5plus_call_to_action button_title=”Click Here to Watch the Video” button_link=”url:https%3A%2F%2Fyoutu.be%2Fw0XoagTkLNo|||” css=”.vc_custom_1608058221792{padding-top: 2px !important;padding-right: 2px !important;padding-bottom: 2px !important;padding-left: 2px !important;}”][/g5plus_call_to_action][/vc_column][/vc_row][vc_row][vc_column][/vc_column][/vc_row]